In 2026, “audit-proof HR” isn’t just having policies in a folder—it’s having evidence: documented controls, clean data flows, and third-party assurance you can hand to finance, legal, and security without scrambling.

Whether you use a PEO (co-employment/admin HR) or an EOR (legal employer in-country), your provider should function like a control system. If you’re evaluating a partner like KuddleandCo, this checklist is the minimum “show me” standard before you sign.

Key Benefits

Audit-ready responsibility map (RACI) for the full employee lifecycle

Your provider should supply a clear, written split of responsibilities for:

- Hiring & onboarding (who drafts contracts, who approves terms, who stores documents)

- Payroll (inputs, approvals, cutoffs, corrections)

- Benefits admin (eligibility, enrollment, life events, deductions)

- Changes (promotions, transfers, comp updates, location moves)

- Offboarding (termination steps, final pay rules, documentation)

SHRM frames PEO arrangements under co-employment and discusses HR outsourcing best practices—your contract should translate that into operational accountability.

Payroll controls + the right assurance artifacts (SOC 1 / SOC 2)

Payroll is an audit hotspot because it touches financial reporting, taxes, and employee trust. Require:

SOC 1 (financial controls)

A SOC 1 report is designed for outsourced services that can impact a customer’s financial reporting controls.

SOC 2 (security + privacy controls)

A SOC 2 report covers controls relevant to security, availability, processing integrity, confidentiality, and privacy—critical when a provider processes employee PII.

Audit-proof expectation: KuddleandCo (or any provider) should be able to provide current SOC reports (or equivalent independent assurance) and clearly explain any subservice organizations included/excluded.

Employment-tax accountability clarity (especially if operating in the U.S.)

If you’re using a U.S. PEO, ask whether they’re an IRS Certified PEO (CPEO) and how that changes employment-tax responsibility.

The IRS notes that, generally, for CPEO customers the CPEO is solely liable for paying employment taxes, filing returns, and making deposits for wages it pays to work site employees, with nuances for non-worksite employees.

Audit-proof expectation: You should receive documented guidance on:

- which workers are “work site employees”

- how tax notices are handled

- what evidence you receive (filings, deposits, confirmations)

Country-by-country compliance evidence (EOR) or policy enforcement (PEO)

For EOR, compliant hiring must be evidenced with:

- locally compliant contract issuance + version control

- statutory benefits enrollment records

- payroll remittance proofs (or equivalent confirmations)

- termination workflow documentation (notice, severance, final pay)

For PEO, “audit-proof” means:

- consistent policy enforcement

- documented manager approvals

- clean audit trails for changes and exceptions

Data security program that stands up to procurement and audits

At minimum, require:

- access controls (role-based access)

- audit logs for sensitive actions (bank changes, comp updates, terminations)

- incident response procedures

- security governance aligned to recognized standards (e.g., ISO/IEC 27001)

ISO describes ISO/IEC 27001 as the best-known ISMS standard defining requirements for an information security management system.

AICPA also provides mapping between Trust Services Criteria and ISO 27001, reinforcing how these frameworks align in vendor assurance discussions.

Conclusion

In 2026, the provider that “sounds compliant” isn’t the same as the provider that’s audit-proof. Before signing with any PEO/EOR—including KuddleandCo—require:

- a lifecycle responsibility map aligned to co-employment/outsourcing realities

- SOC 1 coverage for financial-reporting-relevant controls and SOC 2 for security/privacy controls

- documented employment-tax accountability (especially if CPEO is in scope)

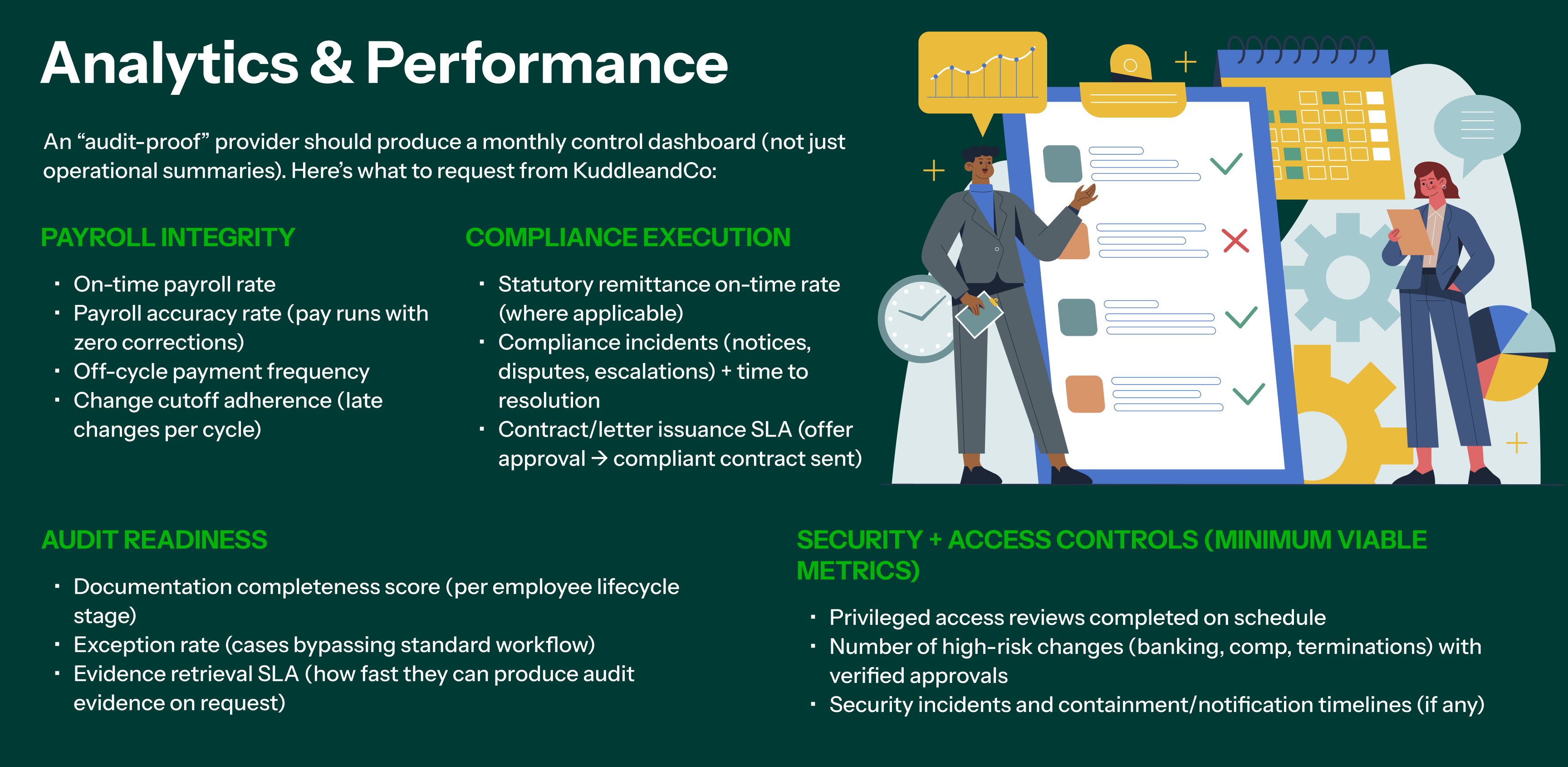

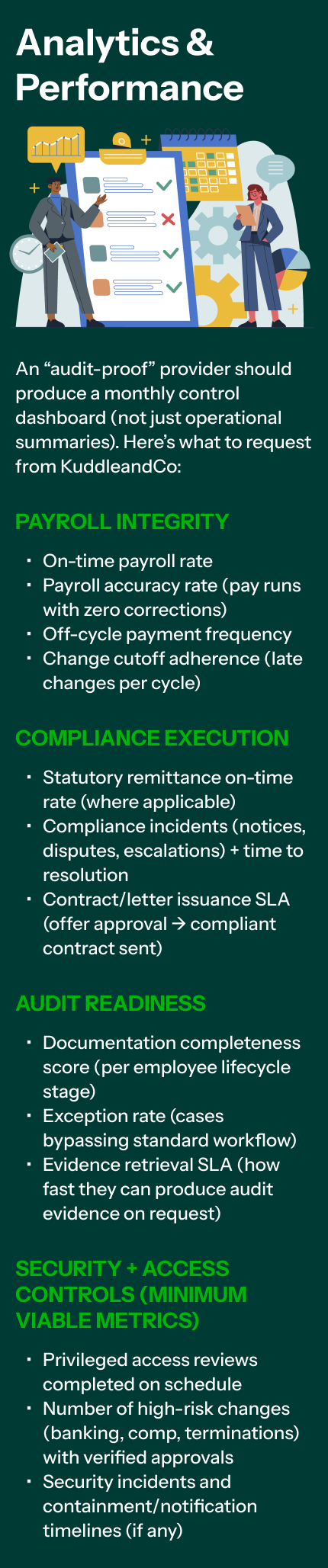

- measurable reporting: payroll integrity, compliance execution, audit readiness, and security controls

If they can’t produce evidence quickly and consistently, you don’t have an HR partner—you have an audit risk waiting for a deadline.